Blame it on Standard Deviation

Bet you thought REITs were boring. Don’t worry, we all did. But they aren’t boring anymore, and unfortunately, for all the wrong reasons.

Earlier this week I posted a thread on twitter about some of the issues facing Blackstone’s BREIT and a couple other private REIT funds, and there is still so much more to say and to understand. Since I’ve been in a jetlag daze while playing catch up all week after a wonderful trip to Thailand, I’m going to break up my commentary into a few smaller posts.

First off, here is the initial twitter thread:

Twitter is great for short form, and I’m going to go deeper on a couple of the concepts I brought up. Two concepts that I plan to explore in more detail are the crowding effect and the liquidity premium, both of which are critical to understanding how we got here and how BREIT fits into the larger picture of our capital markets. For today, I want to kick this off talking about the standard deviation. It connects to BREIT, I promise, so bear with me.

-

Blame it on the standard deviation.

The standard deviation is a simple calculation that measures the dispersion within a data set. You sum the squares of the difference between each data point and the mean and then divide that number by the amount of data points in the set, square root that number and there you go. People like to fancy it up and make it sound more complex than it is but it is actually very simple. If you are on excel it takes as long to calculate as it takes to type =stdev(cell:cell). Yes: stdev. You don’t even have to type the whole words. It is simple.

And it is the cause of so many investing catastrophes, with private REIT funds likely to be the next in a long line of fortunes devastated by the stdev.

Let’s take a moment and consider what’s become of modern investing. Investment decisions are being increasingly centralized. Retail investing tends to be managed by financial advisors, and advisors are increasingly relying on home offices and model portfolios to run the asset management for them. And they are increasingly relying on optimization engines to allocate the capital. And the optimization engines are increasingly relying on one simple definition of risk: stdev.

I suppose it is unfair to blame the standard deviation. Stdev didn’t ask to be confused with risk. We did that.

And that’s the heart of the matter. Risk is forward looking. Stdev is backwards looking. And we’ve confused the two.

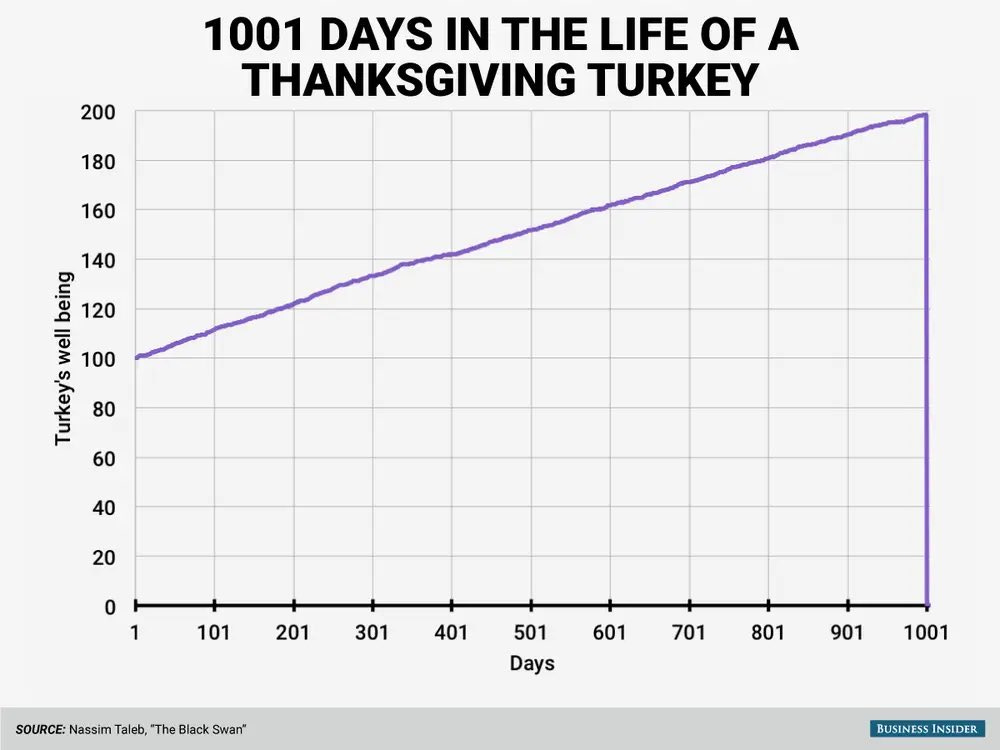

Let’s consider Taleb’s turkey, which itself is a play on Bertrand Russell’s chicken. The turkey is born and well cared for by its farmers. We can chart the turkey’s well-being and we’ll see a nice steady increase over time. And on the day before thanksgiving we can look back and marvel at how low the stdev is, and how low-risk the turkey’s life is. Today’s portfolio optimizers would just love Taleb’s Turkey for even the most conservative retirement account - until Thanksgiving day.

The Blackstone BREIT fund is Taleb’s turkey, which makes the whole thing so sad. The historical risk profile of the fund has skewed it’s current investor base towards the least risk tolerant.

Once you can separate observed/historical risk with unknown/future risk you see it everywhere.

That just happened last night as I was thinking about Taleb’s Turkey and BREIT’s historical versus future expected returns. Risk is everywhere, and there is no reason to expect the historical standard deviations of a fund to mirror the risks around the corner in that fund, strategy, structure, or asset class.