More to Come. That’s how AQR left off their paper on using machine learning to better predict market outcomes. That’s the headline too, as far as I’m concerned. More to come.

It is an exciting time to be exploring systematic alpha in markets. I can hardly believe I wrote that, I can hardly believe I feel that. But it’s true.

Discretionary stock-picking has long been a joke, fundamental analysis has been mocked by tech valuations, factor investing and smart-beta have been mined and packaged and sold with over-promises, to the point where they’ve been destined to under-deliver.

And the steady never-ending bid of index flows along with the self-fulfilling performance that those flows brought have left the investment world well-fed and complacent.

Alpha has become a nostalgic concept, and the pursuit of it met with eyerolls and skepticism.

And now, for the first time in so long, the search for alpha is exciting again. Now we’ve got machine learning modeling that enables complex models. Now, anyone who is paying attention can again say: more to come.

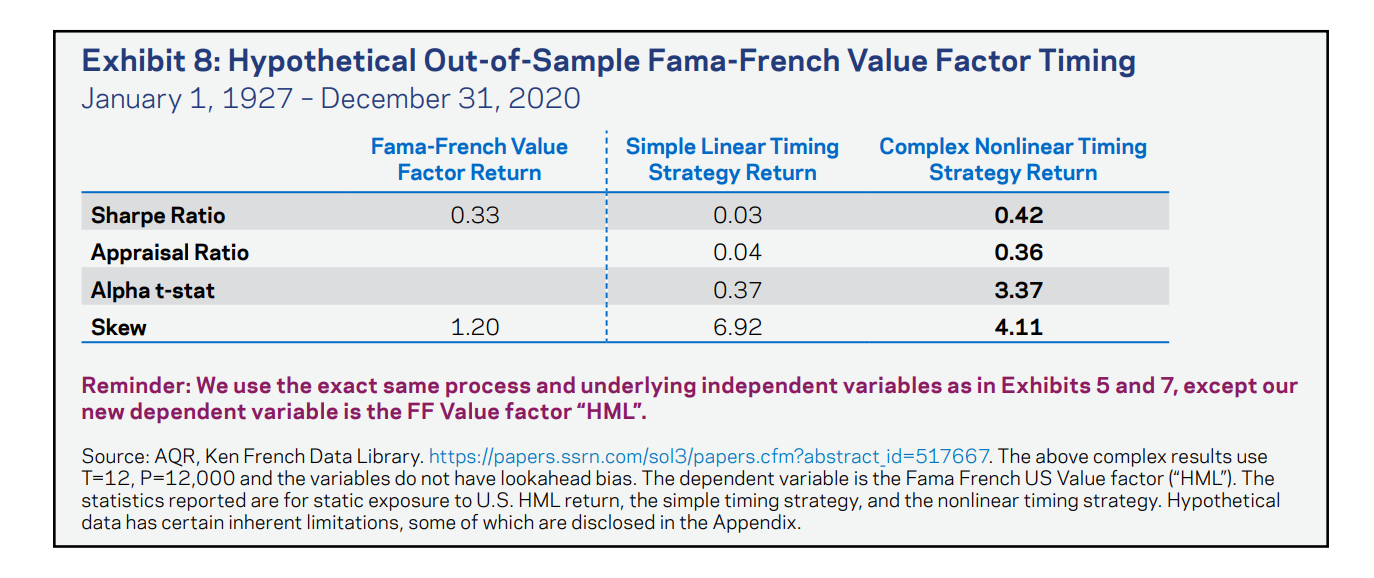

The AQR paper looks at complex modeling, defined as models where the number of predictive variables is larger than the number of return time series observations, and enabled by machine learning.

Machine learning allows the models to identify non-linear relationships between the different variables. If you’ve used simple regression models you might expect that adding variables only adds noise and has a de minimis impact on returns. But that is not the case.

AQR has found that “large, complex models… better estimate the true expected return model, and generate better market timing performance”. The performance improvements were defined as “real but modest”, but let’s think about the “real” and consider how early it is to cap the possibilities as “modest”.

At Armada we’ve found the same. While AQR looked at three applications (timing the stock market, timing the bond market, and long/short value), Armada is focused on just one asset class: real estate.

With the depth of trained data and predictive variables & factors we can now observe, complex models exploring non-linear relationships between them produces a vast ocean of signals. Our job is to reduce that ocean into a small lake, or as my friend Patrick O’Meara describes, a shoreline along that lake.

We’ve been doing just that for our institutional clients, and within our small asset class we have identified real but modest enhancements to expected returns, even when normalizing for parameters such as factors, fit and risk.

So it is an exciting time again for those of us hunting for alpha. Just as we progressed from the abacus to the calculator to spreadsheets to regressions, we are progressing once again and there will be no going back. Anyone rolling their eyes at AI and machine learning and it’s application within portfolio management will be left behind.

More to come.