I’m going to sell you a narrative:

Stocks tend to go up over the long term. Sure there is volatility in the short term, but over the long term you are paid back handsomely for enduring that volatility in the form of an equity risk premium. Time in the market is more important than timing the market, as they say, and what is most important is managing any behavioral biases that tempt you to sell. Oh, and by the way, I’ve got a century of data on my side.

How’d I do? Are you convinced? Now let me try another narrative:

We’ve engineered markets to the breaking point and there is simply no juice left to squeeze out of this lemon. The monetary policies enacted during the global financial crisis - quantitative easing and interest rate manipulation - have been abused in the years since with diminishing returns, while the root causes of the crisis have been left unaddressed. Bond issuers can’t refinance at higher rates, and hyper-inflation can’t be contained at lower rates. And the divergence between financial assets and economic growth over the past decade tells us that a crash and depression are imminent.

The beautiful thing about markets, it takes two sides to make it. It takes two narratives to make a market.

It takes narratives to make a market.

Narratives are the market.

Wait, did I just lose you? Let me back up a bit.

You might think that the value of a stock is a math problem to solve. Or a question of forecasting. And whoever best understands the corporate balance sheet, whoever best calculates the value of it’s assets, whoever best predicts the trajectory of the business will do the best in the market. They’ll be proven right and they’ll be rewarded for being right when the stock price inevitably trues up to the level it should be trading at.

Except “should be” got nothing to do with it.

The weighing machine is broken. The valuation models you memorized for the CFA exam are broken. There is no rational actor coming in to save price discovery and make everything trade as it should. There are only narratives to measure, to capture, and to twist in your direction.

This is the new game of capital markets.

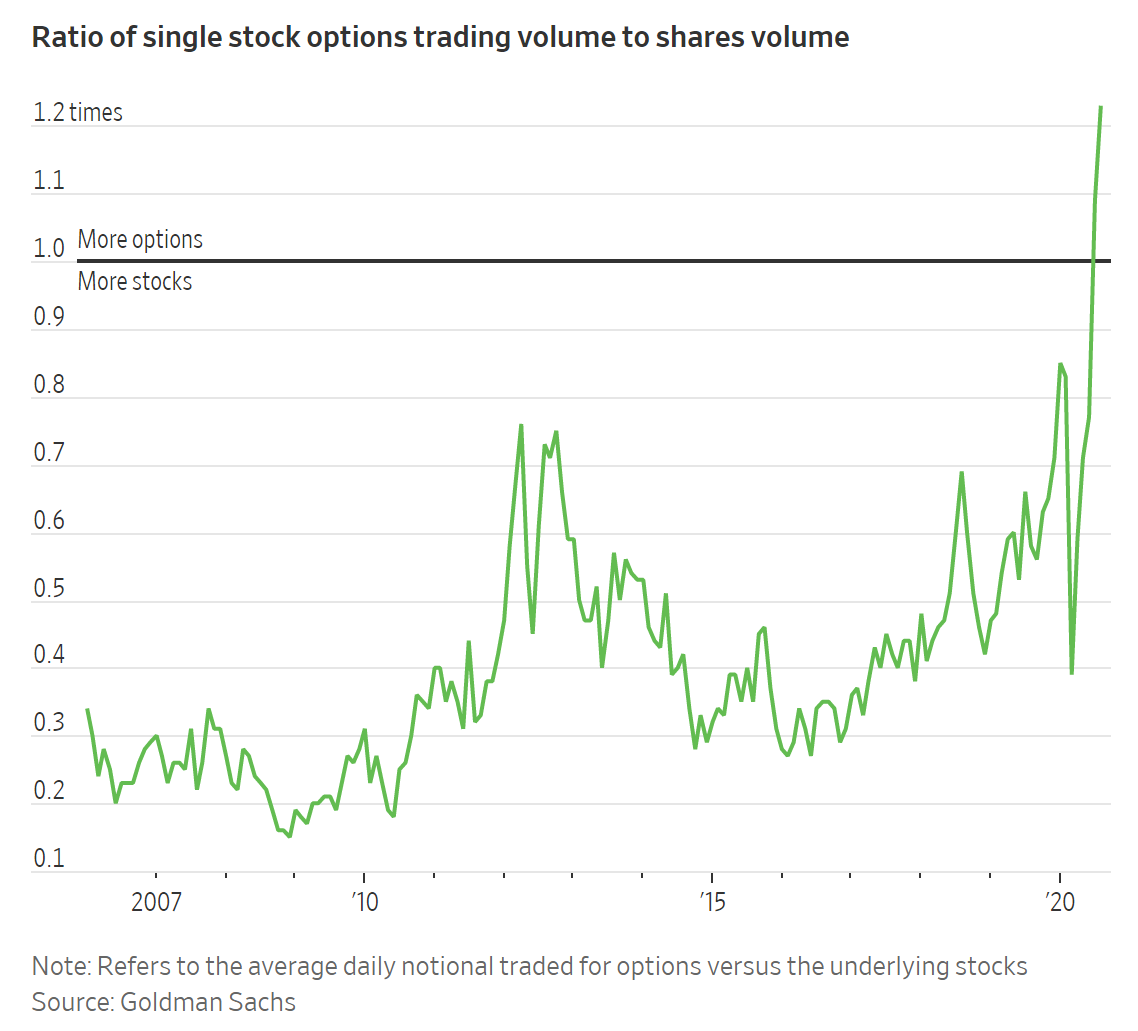

All of this is a long time coming. Ben Hunt has been talking about narratives driving capital markets for years. Michael Green has connected a straight line between the proliferation of passive cap-weighted index investing and diminishing price discovery. And then last year, options volume flipped equity volume.

And just in case you wanted to tell yourself that all these options trades are institutional hedging or some other fairy tale, I present you with new data showing that more than half of all options trades now expire within the same week.

These are bets. The Chiefs -7.5, the over, Josh Allen for MVP, and the Nasdaq to crash on CPI data.

Take all of the sophistication that asset managers like to present, take all of the hours spent acquiring a CFA designation, take all of the stock disclosures, all the 10Ks and 10Qs, all the research reports. Take your Ben Graham books. Throw them all in the trash.

This is what the market is. A bunch of little retail bets driven by the frenzied sentiment of the day. A gambling app.

The other thing that I noticed that's new to me is how retail investors use tools that measure "race conditions" in stocks that show they are being targeted for a squeeze, then those same stocks get more people to buy in if it looks promising and they can create huge very short term bubbles in small float names. It's just another table in the gambling hall.